The Short Version

RMDs (Required Minimum Distributions) are required withdrawals from pre-tax retirement accounts (also known as tax-deferred accounts) starting at age 73 (75 if you were born in 1960 or later).

They are taxed at ordinary-income rates and are mandatory, with stiff penalties if you don’t take them as required.

Reality Check

The IRS always gets its cut. When you contribute to a traditional IRA, you don’t pay taxes on that contribution. In fact, you likely get a tax deduction in the year you make it. When you invest your IRA contributions (in stocks, bonds, mutual funds, ETFs, money markets, etc), you are not taxed on any gains those investments realize through price increases, dividends, or interest. Yet…

Remember, the IRS always gets its cut. You don’t initially pay taxes on IRA and other pre-tax retirement contributions and their growth. You will pay taxes when you take a distribution from it.

But what if you don’t need the money from a distribution? What if your Social Security benefit, pension, and other sources of income provide you with more than enough funds to cover your expenses?

The IRS doesn’t care. They want their share, and they are going to take it whether you need it or not. You are forced to take a distribution, a Required Minimum Distribution (RMD), when you reach a certain age. Because… the IRS always gets its cut. Short of committing tax evasion or fraud, you have no choice.

“But that’s not fair!” Maybe not. As my parents (and their parents) always said, “Sometimes life isn’t fair.” I often add, “The IRS is never fair.”

Fortunately, there are ways to minimize the tax consequences of RMDs.

IMPORTANT NOTE: Retirement accounts, including RMDs, are governed by the Federal tax code. As such, the rules and requirements can be changed at any time. Always check the tax code (preferably with professional assistance) before making any changes to anything that could have tax consequences.

What an RMD Is

An RMD is a Required Minimum Distribution that must be withdrawn from certain IRA accounts at certain times.

Types of tax-deferred accounts are listed below. Each year, you must withdraw a minimum amount based on a formula that includes: your tax-deferred account balances; your age, and an IRS factor called a Life Expectancy Factor.

The formula to determine your RMD amount is: Year-End Tax-deferred Account Balance ÷ “IRS Life Expectancy Factor.” That factor changes every year, because your life expectancy changes every year.

You can read all about RMDs —which accounts require them, which don’t, and what and how the “Life Expectancy Factor” is determined by reading IRS Publication 590-B.

Here’s the problem with IRS Publication 590-B… It’s about 35,000 words. That’s a 100-page book. Depending on how fast you read, it’ll take you 2 – 4 hours. And that’s just reading the words. The whole thing is full of IRS Speak, a confusing language that normal people can’t comprehend well.

Fortunately, sane people have developed calculators to help you understand what your RMDs will be over time.

One of the better RMD calculators I’ve found is on a website called Dinkytown (I know, weird name). They have around 400 financial calculators available, are highly regarded within the financial community, and are embedded on many leading financial websites. I’d embed one on this site, but they want $170 to do that, and I’m retired and living on a (mostly) fixed income.

You can, however, use any Dinkytown calculator for free on their website.

Here is the Dinkytown RMD Calculator. Enter a few bits of info (your & your spouse’s age and tax-deferred account balances. You can (and should) also enter a hypothetical rate of return for your tax-deferred accounts. Why? Because you might be making RMDs for 20 years. Your tax-deferred accounts will be growing during that entire period, which means your RMD amount will also grow. The calculator defaults to 4%. Personally, I use 6% (and look at changes at 10-12%), because no one can predict future return rates, and I want to see worst-case examples.

When Do RMDs Start?

Age 73, or 75 if you were born in 1960 or later

Your first RMD is due by April 1 of the year after you turn 73 (or 75, depending on your birth year). Be very careful if you plan to take your first RMD between Jan 1 and April 1 of the year after RMDs start. Why? Because you will be required to take a second RMD before December 31 of that year, too. After your first year of RMDs, subsequent yearly RMDs are due by December 31. Taking two years of RMDs in a single calendar year will increase your taxes for that year, perhaps significantly.

Here’s an example

I was born in 1960. That means I have to start taking RMDs the year I turn 75, which would be 2035.

My first-year (2035) RMD amount would be based on the total balances of all tax-deferred accounts as of December 31, 2034. Those distributions (which are the same as withdrawals) would have to be made by December 31, 2035. BUT, for your first RMD (and only the first one), the IRS will graciously allow me to delay that first-ever RMD withdrawal until April 1, 2036.

Here’s the problem with taking that delay… My 2036 RMD is also due by December 31, 2036. So if I delay my first-ever RMD after Dec 31 (up until the allowed April 1 date), I will be required (that’s the “R” in RMD) to take a second withdrawal on or before December 31.

And every dime of any RMD is taxed at ordinary income rates. I struggle to think of any situation where someone would want to be taxed on two RMDs in one calendar year.

Accounts Affected

- Traditional IRAs: Individual retirement accounts.

- Rollover IRAs: IRAs holding funds rolled over from qualified plans.

- SEP IRAs: Simplified Employee Pension plans.

- SIMPLE IRAs: Savings Incentive Match Plans for Employees.

- 401(k) Plans: Traditional (pre-tax) company plans.

- 403(b) Plans: Tax-sheltered annuities for non-profits.

- 457(b) Plans: Deferred compensation plans for state/local government employees.

- Profit Sharing Plans: And other defined contribution plans.

- Keogh Plans: Plans for self-employed individuals.

- Inherited IRAs/Roth IRAs: Beneficiaries must take RMDs

Note: Roth IRAs are NOT on this list.. Unlike the tax-deferred accounts listed above, Roth contributions are taxed when you make them. Growth inside Roths is distributed tax-free. There is no RMD requirement for Roth IRAs.

RMD Increase over Time Example

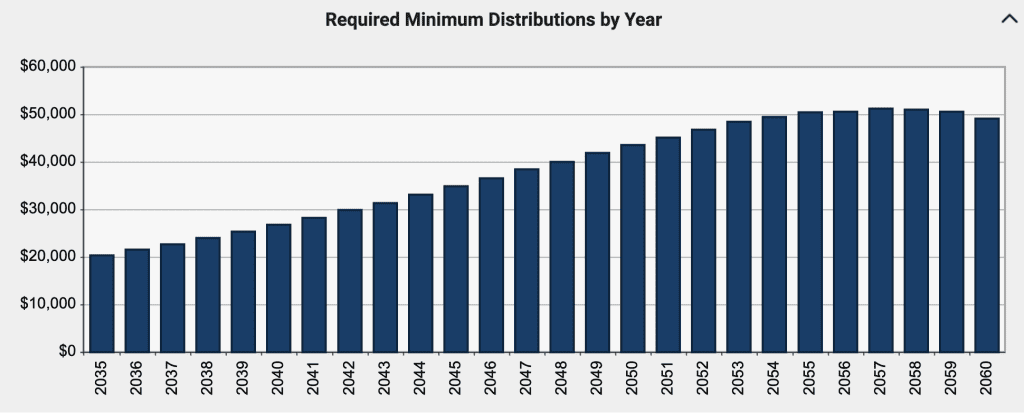

Let’s say you have $500,000 in tax-deferred accounts. You were born in 1960 or later, so your RMDs begin the year you turn 75.

Age 75 → RMD ≈ $37K

That’s $37,000 in taxable income, whether you need it or not.

Here’s an example of predicted RMDs from ages 75 to 100 for a $500K tax-deferred balance with a rate of return of 6%. This chart shows RMDs for someone born in 1960 who would begin RMDs in 2035:

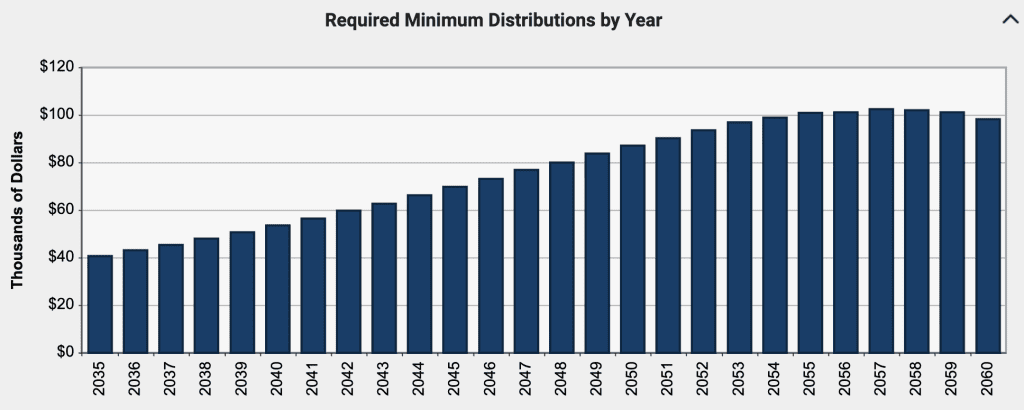

And here’s the same for a $1M balance:

RMDs increase over time due to portfolio growth, and reduced life expectancy.

Why RMDs Matter

An RMD isn’t just a withdrawal. It’s taxable income — and it lands on top of everything else you’ve already got coming in.

That distinction matters more than most people realize until it’s too late to do much about it.

They can push you into a higher tax bracket

If you’re already collecting Social Security, drawing from a pension, or taking other distributions, your RMD gets added to all of it. Combined, that income can nudge you — or shove you — into the next tax bracket.

And because RMD amounts tend to grow over time (your accounts keep compounding even as you withdraw), this isn’t a one-year problem. It’s a creeping, annual problem that gets larger as you age.

They increase Social Security taxation

Here’s something that surprises a lot of people: up to 85% of your Social Security benefit can be subject to federal income tax, depending on your combined income.

RMDs count toward that calculation. A large enough RMD can push you past the threshold where more of your Social Security becomes taxable — effectively creating a double hit. You’re taxed on the RMD, and suddenly more of your Social Security is taxable too.

They can trigger IRMAA — and that’s a big deal

IRMAA stands for Income-Related Monthly Adjustment Amount. It’s the Medicare surcharge that applies when your income exceeds certain thresholds — and it’s based on your income from two years prior.

So an RMD that pushes your income over a bracket threshold in 2025 shows up as higher Medicare premiums in 2027. Every year, tens of thousands of retirees get hit with this and don’t connect the dots back to their RMD.

The surcharges aren’t trivial. Depending on how far over the threshold you land, IRMAA can add hundreds — or over a thousand — dollars per month to your Medicare costs.

We go deeper on IRMAA and how to manage it here.

They reduce your flexibility

This one is less about dollars and more about control.

When you’re taking RMDs, the IRS is setting part of your withdrawal schedule for you. You may not need the money. You may not want the income that year. You may have preferred to let those funds keep growing. Doesn’t matter. The distribution is required, it’s taxable (as ordinary income), and it has to happen on the IRS’s timeline — not yours.

That loss of flexibility becomes more significant when you’re trying to manage your tax picture carefully across a long retirement. Every mandatory withdrawal is one less lever you control.

Interested in getting new articles in your email?

Penalty

You don’t want to miss making a Required Minimum Distribution. Penalties can be steep — up to 25% of the amount that should have been withdrawn (the RMD amount) but was not. Miss a $50,000 RMD, and now you have to pay a $12,500 penalty. And of course, this is on top of the RMD. So you’d still have to make the $50K RMD, and write the IRS a check for another $12,500…

You must file IRS Form 5329 to report the penalty, though you can request a waiver if the failure was due to reasonable error. Of note, “I forgot” is not considered a “reasonable error” by the IRS. Things like administrative error by a financial institution, serious illness, mental incapacity, or death in the family might be considered a reasonable error by the IRS, and they might reduce or waive the penalty. They will not waive the actual RMD. The IRS always gets its slice of your pie.

Strategies

The good news: you have more control over RMDs than it might feel like. Not over whether you take them — that’s settled. But over how, and when, and how much damage they do.

Take them early — or spread them out

Most people wait until late in the year to take their RMD. There’s no rule that says you have to. You can take the full amount in January. You can spread it across monthly withdrawals. You can take it in pieces whenever it suits your cash flow.

Why does timing matter? Because a large RMD taken late in the year can push you into a higher tax bracket for that year — and might affect your Medicare premiums two years out through IRMAA. Taking distributions earlier, or spreading them, gives you more visibility into your tax picture before the year closes.

Use them intentionally

Here’s where people leave money on the table. They take the RMD, it lands in their checking account, and it just sits there — or gets spent.

A better move: treat the distribution as a decision, not just a transaction. You could reinvest it in a taxable brokerage account. You could use it to fund a Roth conversion (more on that below). You could gift it to family members or a charity in a tax-efficient way. The point is — the money has to come out. What you do with it after is still up to you.

Plan ahead — before you hit 73 (or 75)

The biggest mistake people make with RMDs is treating them as a future problem. They’re not. They’re a future outcome of decisions you’re making right now.

If you’re in your 60s with significant pre-tax balances, every year you delay thinking about this is a year you’re not managing it. The accounts keep growing. The future RMDs get larger. The tax bill gets bigger.

Running even a rough projection — using something like the Dinkytown calculator mentioned earlier — can be eye-opening. Most people are surprised by how large RMDs get by their late 70s and 80s.

Smarter Moves

These aren’t tricks. They’re legitimate strategies that can meaningfully reduce the tax impact of RMDs — if you plan early enough to use them.

Roth Conversions

This is probably the most powerful tool available to people in the years before RMDs begin.

Here’s the logic: every dollar you convert from a traditional IRA to a Roth IRA reduces your future RMD base. Smaller pre-tax balance = smaller RMDs = less forced taxable income later.

Yes, you pay taxes on the amount you convert in the year you do it. But you’re choosing when to pay, and how much — instead of letting the IRS decide for you at 75, 80, or 85.

The sweet spot for conversions is typically the gap between retirement and when RMDs (and Social Security) kick in. Income is often lower in those years, which means you may be converting at a lower tax rate than you’d face later.

This doesn’t work for everyone. If you’re already in a high bracket, or if you need the converted funds soon, the math may not hold up. But for many retirees, a multi-year Roth conversion strategy is worth a serious conversation with a tax professional.

Here’s a deeper look at Roth conversions and how to think about them.

QCDs — Qualified Charitable Distributions

If you’re charitably inclined and over 70½, this is one of the cleanest tax moves available.

A QCD lets you transfer money directly from your IRA to a qualified charity — up to $105,000 per year (2025 limit, indexed for inflation). That distribution counts toward your RMD, but it never shows up as taxable income.

Compare that to the alternative: take the RMD, pay taxes on it, then write a check to charity and maybe get a deduction if you itemize. A QCD skips the taxable income step entirely.

If you’re donating anyway, this is almost always the better approach.

A few requirements: the money must go directly from the IRA to the charity — you can’t withdraw it yourself and then donate it. The charity must be a qualifying 501(c)(3). And QCDs don’t apply to SEP or SIMPLE IRAs that are still active. Check with your IRA custodian and tax advisor before setting one up. Schwab has a good overview of QCDs here (as does Fidelity, and other investment brokerages and financial institutions).

Multi-Year Tax Planning

Required Minimum Distributions don’t exist in a vacuum. They interact with everything else: Social Security income, capital gains, IRMAA brackets, your standard deduction, potential estate planning goals.

That’s why the smartest RMD strategy isn’t a one-year fix — it’s a multi-year plan. Some things worth mapping out:

- At what income level do you cross into the next IRMAA tier?

- Is there a bracket gap you can fill with Roth conversions before RMDs start?

- How does your RMD income interact with Social Security taxation?

- What does your tax picture look like if one spouse passes away and filing status shifts to single?

These aren’t simple questions. But they have answers — and the people who think through them in advance tend to pay a lot less in taxes than those who don’t.

Bottom Line

Required Minimum Distributions aren’t terribly complicated.

But they are consequential. A large, unmanaged RMD can push you into a higher tax bracket, trigger extra Medicare premiums, and reduce your flexibility — year after year, for potentially two decades.

The rules are what they are. The IRS built this system, and you’re playing by their rules whether you planned for it or not. You don’t have to, and probably won’t, like it.

What you can control is how you prepare. Start running projections. Look at Roth conversions during your lower-income years. Consider QCDs if you’re giving to charity anyway. Get a tax advisor involved before the RMDs start — not after.

Plan early, or they plan for you.

The retirees who pay the least in taxes didn’t get lucky. They just started thinking about this sooner.

The link below is an affiliate link. If you use it, I may earn a small commission — no extra cost to you.

Personal Note: I use the paid "PlannerPlus" version of Boldin, a terrific product for financial planning. It's the best tool I've found (and I've tried a lot) for financial and scenario planning, including: RMDs, RMD conversions, Monte Carlo analysis, investments, income, expenses, Social Security, benefits, taxes, real estate, and more. Boldin also has very good courses, educational materials, and customer support. I can not recommend it highly enough.

4 comments

Hi Jay! We’re in the “transferring the 401k into a Roth” stage, and the ordinary income taxes on the transactions are killer! Our accountant has determined what our sweet spot of yearly conversions should be but I wish we’d started this earlier! We’re 69 and 70 and have been doing this for a few years now.

Another factor is the high IRMAA on Medicare because income during the transition is much higher.

Hi Lisa!

Feeling your pain. I wish we’d started Roth conversions (and contributions) 20 years ago. We’re not “of age” yet, still 10 years away, but it sure would have been simpler (and easier to afford) if we’d gotten an earlier start.

We have yet to feel the wrath of “Aunt IRMAA,” but it’s only a matter of time… I’ve touched on IRMAA in a few posts here, but it needs more depth. That will be coming soon.

Hope y’all are well! Francyy says “Howdy”. We’re headed out on our mutual Windstar friends’ boat in a few weeks (Rome –> Croatia –> Venice).

Best to you both, and thanks for reading and commenting!

Excellent advice, as always, Jay.

We opted to take our RMD monthly rather than in a lump sum.

Withdrawing monthly evens out our cash flow. Our IRA is mostly in stock and mutual funds, so it also smooths out the vagaries of the market.

Ira Serkes

Thanks, Ira!

We’re not at RMD age yet, but spreading them out is our plan too. Have a few years available for Roth conversions, too. It can be pricey paying the IRS, but it really boils down to “Pay me now or pay me later.” Might as well pay it now when we at least have a little more control of it.

Appreciate you reading and commenting!