The word “retirement” implies a clean break. You work, and then you stop working. Full stop.

But that’s not how it plays out for a growing number of retirees. Somewhere between fully employed and fully retired, there’s a middle ground that a lot of people find genuinely works better.

Part-time work. Consulting. Freelancing. Seasonal work. A small business on the side.

Some people do it for the money. Some do it for the structure. Some do it because they miss having somewhere to be. Some stumble into it almost by accident and find it fits better than full retirement ever did.

This isn’t the right path for everyone. But it’s worth thinking about clearly, because the reasons to consider it go well beyond the paycheck.

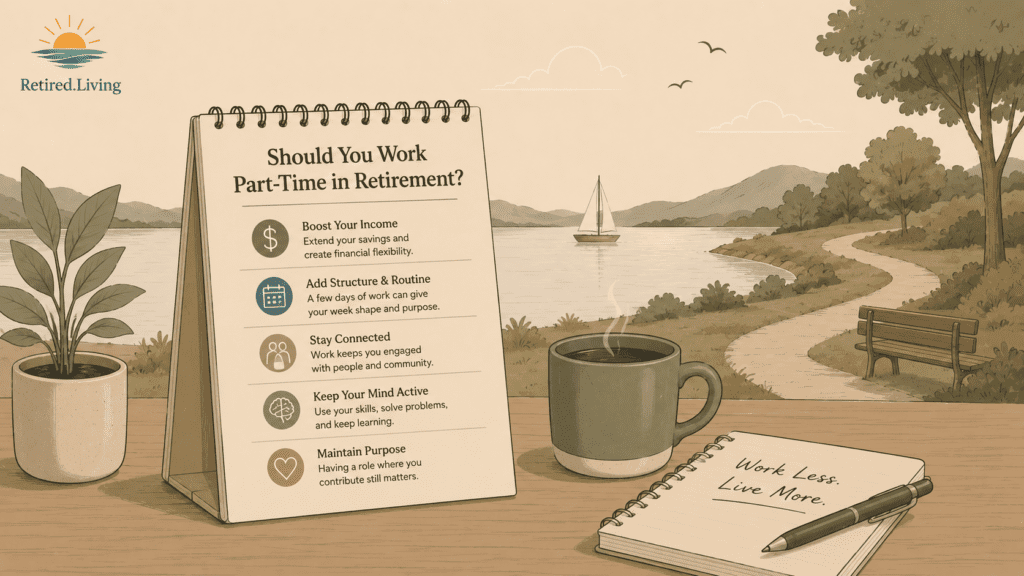

The Financial Case

Start here, because for many retirees it’s the most concrete reason.

Every dollar you earn in retirement is a dollar you don’t have to pull from savings. In practical terms, even modest part-time income can meaningfully extend the life of a portfolio, especially in the early years of retirement, when sequence-of-returns risk is highest.

Here’s a simple example: if you’re withdrawing $60,000 a year from savings and you earn $15,000–$20,000 from part-time work, you’ve reduced your annual withdrawal by 25–30%. Over a 20–30 year retirement, that difference compounds significantly.

Part-time income also gives you flexibility. Market down? Pull less from savings and lean on the earned income. Unexpected expense? You have a cushion that isn’t your portfolio.

There are wrinkles, though. A few to be aware of:

Social Security and earned income. If you claim Social Security before full retirement age and continue working, your benefits may be temporarily reduced if you earn above a certain threshold. In 2024, that limit was $22,320. Once you hit full retirement age, the earnings limit disappears. The Social Security Administration has current figures — worth checking if this applies to you.

Medicare IRMAA. Higher income in retirement can push you into higher Medicare premium brackets. Part-time income adds to your MAGI, which determines IRMAA. If you’re near a bracket threshold, it’s worth running the numbers.

Taxes. Earned income in retirement is still taxable. How it interacts with Social Security, RMDs, and other income sources depends on your overall picture. This is a good conversation to have with a tax professional before you take the leap.

The Non-Financial Case

This is where it gets interesting, because for a lot of retirees, the money ends up being secondary.

Part-time work addresses several of the things that make full retirement harder than expected:

Structure. Two or three days a week of work gives your schedule shape. You know what Tuesday looks like. There’s somewhere to be.

Social connection. Work puts you around people. That matters more than most people anticipate until it’s gone.

Identity and purpose. This is quieter, but real. Having a role — something you’re responsible for, something where your effort matters — addresses the identity loss that a lot of retirees feel after leaving full-time work.

Mental engagement. Staying cognitively active in retirement matters for brain health. Work is one way to do that, especially if it involves problem-solving, learning, or complex tasks.

None of these require a paying job. You can get all of them from volunteering, serious hobbies, or community involvement. But for people who find those alternatives less compelling, part-time work is a natural and often underrated option.

Types of Part-Time Work Worth Considering

Not all part-time work is created equal in retirement. A few categories to think about:

Consulting in your former field. Often the path of least resistance. You have expertise that’s valuable, and you can typically set your own hours and terms. The main risk: it can feel too much like the job you just left.

Flexible or seasonal work. Retail during the holidays. Tax preparation. Tourism-related work. These tend to be low-pressure with clear start and end dates, which suits some retirees very well.

Teaching or tutoring. If you have knowledge worth sharing, this can be deeply satisfying. Community colleges, adult education programs, and tutoring platforms all offer opportunities.

Turning a hobby into income. Woodworking, photography, writing, landscaping. Not everyone wants to monetize a hobby, and there’s a real risk of ruining something you love by making it work. But for some people, it’s a natural fit.

Part-time roles with benefits. Some employers — notably Costco, Home Depot, Starbucks, and others — offer benefits including health coverage to part-time employees. For retirees who retire before Medicare eligibility at 65, this can be financially significant.

Here’s the Catch

A few honest tradeoffs to consider.

It can delay the transition you actually need to make. For some retirees, staying in partial work mode is a way of avoiding the harder work of figuring out what retirement actually looks like. If you’re considering part-time work because you genuinely don’t know what else you’d do with your time, that’s worth sitting with. The answer might be to work part-time, or it might be to do the harder work of designing a retirement life that doesn’t require an escape hatch.

Your former employer may complicate things. Consulting back to a previous employer raises questions about independence, scope creep, and whether you’ve really left. Some retirees find it works beautifully. Others find themselves gradually pulled back into full-time commitments without full-time compensation.

Not all income is worth the tradeoff. If a part-time role is stressful, inflexible, or feels like an obligation rather than a choice, it can undermine the things that make retirement good. Low pay with high stress is a bad trade at any age.

It can complicate the financial picture. Beyond IRMAA and Social Security interactions mentioned above, earned income in retirement can affect your tax bracket, Roth conversion strategy, and ACA subsidy eligibility if you’re pre-Medicare. Worth modeling before you commit.

A Question Worth Asking Yourself

Before deciding, sit with this: what am I actually solving for?

If it’s income — how much do you need, and is this the most efficient way to get it?

If it’s structure — could you get that from something other than paid work?

If it’s purpose or identity — is part-time work genuinely the answer, or is it a bridge while you figure out what that actually looks like?

None of these are trick questions. Part-time work might be exactly the right answer to all of them. But knowing which problem you’re solving makes it easier to find the right solution.

The Practical Takeaway

Part-time work in retirement isn’t a fallback for people who didn’t save enough. For a lot of retirees, it’s a genuine lifestyle choice that improves both financial security and day-to-day quality of life.

The key is going in with clear eyes — understanding the financial interactions, being honest about what you’re really looking for, and making sure the work you take on is something you’re choosing, not something that’s choosing you.

Done right, a few hours of meaningful work each week can be one of the better parts of retirement.

Related on Retired.Living:

1 comment

“Every dollar you earn in retirement is a dollar you don’t have to pull from savings.”

Very true … and also consult with your financial advisor how much your Individual Retirement Account IRA (Ira IRA for me) requires you to take out every year as an Required Minimum Distribution (RMD).

We decided to take our RMD in monthly installments (rounded up to the nearest $50 or $100) rather than as a lump sum. It smooths our monthly expenses.

IRA (formerly known as Ira)