Retirement isn’t a single decision. It’s a structure.

When I retired at 57, I quickly realized something most financial commercials skip: retirement isn’t just about having “enough money.” It’s about building something stable enough to hold real life.

Over time, I began organizing what I was learning into six core categories. Not because frameworks are trendy, but because retirement touches more than one lever at a time. Pull the wrong one, and something else shifts.

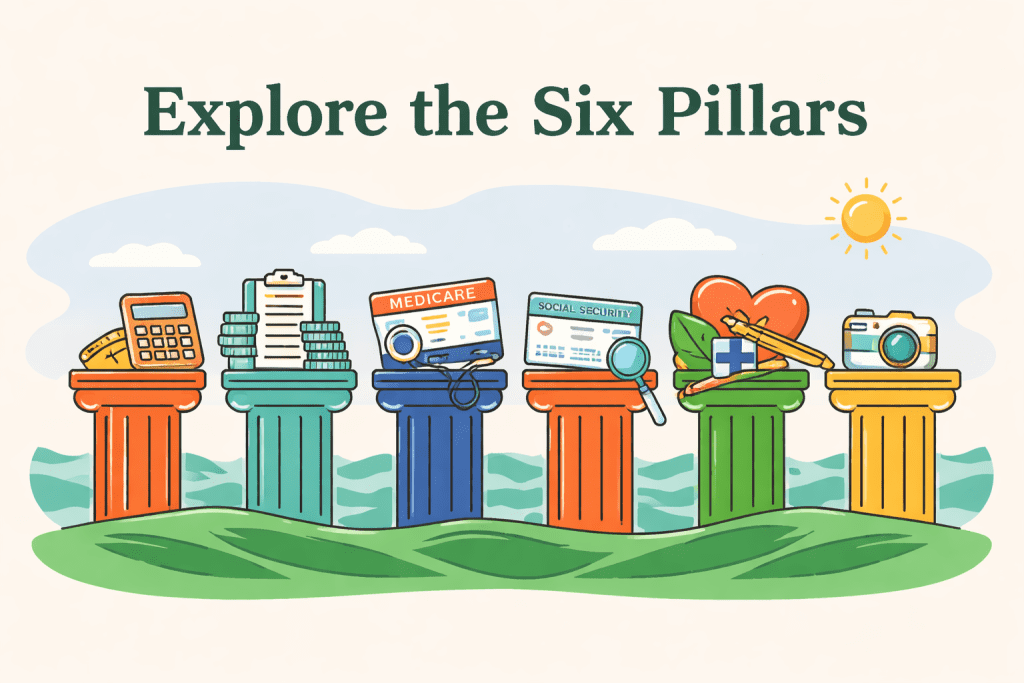

These are the Six Pillars that support everything here at Retired.Living.

Income

Income is the foundation. If the cash flow wobbles, everything wobbles.

This pillar explores:

- Withdrawal strategies

- Portfolio structure

- Roth conversions

- Sequence-of-returns risk

- Social Security timing

- Building reliable income without losing sleep

Not theory. Real-world planning decisions. The kind that determine whether you’re calm… or refreshing your brokerage app every 12 minutes.

Taxes

Taxes don’t disappear in retirement. In some ways, they get more interesting.

Here we break down:

- How your 1040 really works

- Capital gains strategy

- Roth conversion tax planning

- IRMAA thresholds

- RMD timing

- Multi-year tax projections

Because retirement tax planning isn’t about this year. It’s about the next 20.

Medicare

Medicare feels simple until you try to choose.

This pillar covers:

- Parts A, B, C, and D (and what they actually mean)

- Medigap vs. Advantage

- Enrollment timing

- IRMAA surcharges

- Drug plan selection

The goal isn’t to overwhelm you. It’s to help you make informed decisions without needing a decoder ring.

Social Security

When to claim might be the most misunderstood decision in retirement.

We explore:

- Early vs. full vs. delayed benefits

- Spousal considerations

- Survivor strategy

- Break-even analysis

- How Social Security fits into broader income planning

This isn’t about maximizing a check in isolation. It’s about optimizing your entire plan.

Healthcare

Healthcare planning is not the same as Medicare planning.

This pillar looks at:

- Long-term care considerations

- Health savings strategy

- Lifestyle impact on health costs

- Preventive planning

- Navigating the system without losing your mind

Because health isn’t just a line item. It’s leverage.

Lifestyle

This is the pillar most spreadsheets ignore.

Lifestyle includes:

- Purpose after the career chapter closes

- Side projects and consulting

- Travel and hobbies

- Relationships

- Designing days that feel intentional

You can retire financially secure and still feel unmoored. This pillar exists so that doesn’t happen.

Why Six?

Because retirement decisions don’t live in silos.

A Roth conversion affects taxes and Medicare premiums. Social Security timing affects income stability. Healthcare costs affect lifestyle choices.

Everything connects.

The Six Pillars give us a way to talk about those connections clearly and practically, without pretending retirement is one big math problem or one long beach vacation.

Where to Start

If you’re new here, start with the pillar that feels most urgent right now.

- Worried about running out of money? Start with Income.

- Trying to reduce future tax pain? Go to Taxes.

- Approaching 65? Medicare is calling your name.

- Feeling restless in retirement? Lifestyle might be your quiet question.

There’s no perfect order. Just forward motion.

Retirement isn’t about stepping away.

It’s about building something that holds.

Welcome in.