Quick Summary: Retirement doesn’t automatically mean lower taxes. While earned income may disappear, taxable income often continues through IRA withdrawals, Social Security, and Required Minimum Distributions (RMDs). Add bracket compression for surviving spouses and Medicare premium surcharges, and many retirees find themselves paying similar — or even higher — tax rates than expected. Retirement changes your tax structure. It doesn’t eliminate it.

“I’ll be in a lower tax bracket when I retire.”

That line gets repeated so often it feels like a rule.

It isn’t.

Sometimes it’s true. Often it’s not.

The logic sounds simple:

No job → no paycheck → lower income → lower taxes.

But retirement income doesn’t disappear.

It just changes form.

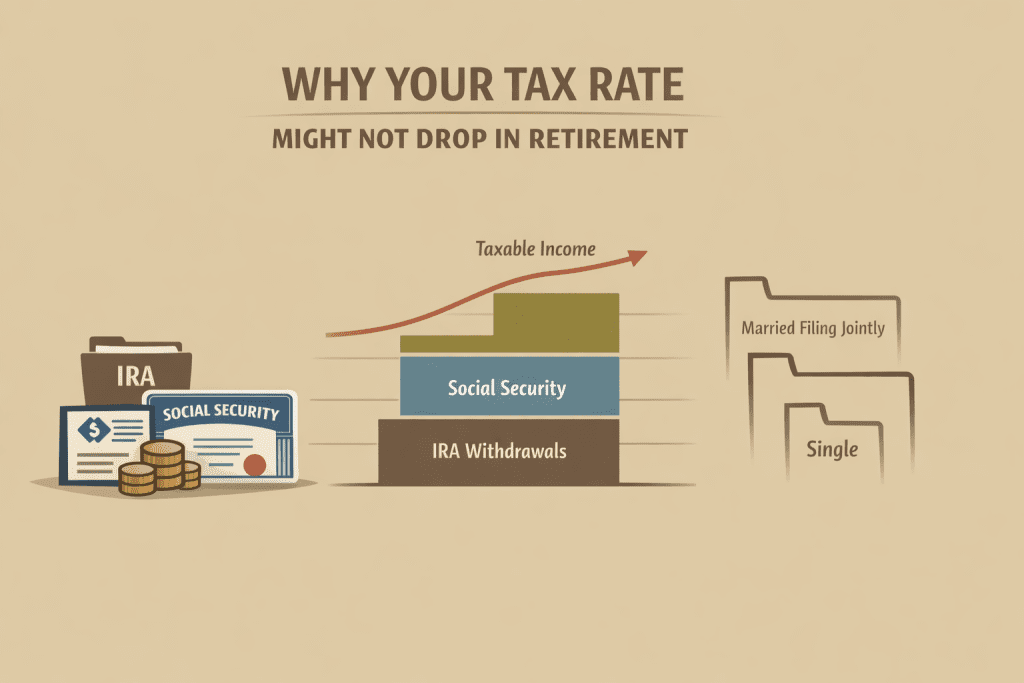

The Illusion of “Lower Income”

When you retire, your W-2 income likely drops to zero.

But taxable income can still come from:

- Traditional IRA withdrawals

- 401(k) distributions

- Required Minimum Distributions (RMDs)

- Social Security

- Capital gains

- Interest and dividends

You may not be working.

But the IRS still sees income.

And in many cases, more than you expect.

The Big Three Surprises

1. Required Minimum Distributions (RMDs)

If you saved aggressively in traditional retirement accounts, you created future taxable income.

Once RMDs begin (currently age 73 for many retirees, 75 for younger cohorts), the IRS requires withdrawals from traditional IRAs and 401(k)s.

You don’t get to decide whether you need the money.

The IRS decides it’s taxable.

If you have $1 million in traditional IRAs, your RMD at 75 could easily exceed $40,000 per year.

That’s forced income.

And it stacks on top of everything else.

2. Social Security Isn’t Automatically Tax-Free

Up to 85% of your Social Security benefit can be taxable.

Not because you’re wealthy.

Because of the provisional income formula.

Other income — especially IRA withdrawals — can cause more of your Social Security to become taxable.

That creates what feels like a hidden marginal tax rate.

One additional dollar of IRA withdrawal can:

- Be taxable itself

- Trigger additional Social Security taxation

That stacking effect surprises retirees every year.

3. The Widow(er)’s Tax Shift

Married couples enjoy wider tax brackets.

When one spouse dies, the survivor files single.

Same assets.

Same income sources.

Smaller brackets.

That means:

- Higher marginal rates

- Faster bracket compression

- Potential Medicare premium surcharges (IRMAA)

The tax code tightens at exactly the moment life may already feel heavy.

Few people plan for that shift.

They should.

A Simple Example

Let’s walk through a very common retirement profile.

Retired Couple at Age 75

| Income Source | Annual Amount | Taxable? |

|---|---|---|

| Required Minimum Distribution | $40,000 | Yes |

| Social Security | $40,000 | Up to 85% taxable |

| Investment Income | $20,000 | Yes (interest/dividends/gains) |

| Total Income | $100,000 | Mostly taxable |

That’s $100,000 of income without working a single day.

That doesn’t look like “low income.”

And remember — if the IRA grows, the RMD grows.

Retirement doesn’t automatically shrink income.

It reshapes it.

Retirement Taxes Don’t Spike — They Creep

Taxes in retirement often unfold in phases:

- Early retirement: lower income, high flexibility

- Social Security begins

- RMDs begin

- Filing status eventually changes

Each stage layers onto the next.

If you don’t plan the transitions, they stack.

Where Planning Makes a Difference

This isn’t about fear.

It’s about sequencing.

Some strategic levers:

- Roth conversions during lower-income years

- Managing capital gains timing

- Coordinating Social Security start dates

- Diversifying tax buckets (taxable, traditional, Roth)

The years between retirement and RMD age are often the most flexible from a tax standpoint.

Once RMDs begin, flexibility narrows.

The Real Risk Isn’t High Taxes

The real risk is assuming taxes will naturally fall — and doing no planning because of that assumption.

Many retirees find themselves:

- In similar brackets as their working years

- Paying higher Medicare premiums due to IRMAA

- Triggering more Social Security taxation than expected

Not because they failed.

Because they assumed.

A Better Question

Instead of asking:

“Will my taxes be lower in retirement?”

Ask:

“When will my income be lowest — and how can I use those years strategically?”

That shift changes everything.

Retirement can absolutely bring lower taxes.

But not automatically.

It takes design.

And design beats assumption every time.

A Practical Note About Taxes

Tax laws change. Individual situations vary. The examples here are simplified to illustrate concepts, not to provide personalized tax advice. Before making decisions about withdrawals, Roth conversions, or tax strategy, it’s wise to consult with a qualified tax professional who can review your specific income sources, filing status, and long-term goals.