Quick Summary: Social Security isn’t automatically tax-free. Depending on your total income, up to 85% of your benefit can be taxable. The formula — called provisional income — includes IRA withdrawals, investment income, and even tax-exempt interest. The surprise isn’t that Social Security can be taxed. The surprise is how easily you cross the thresholds.

“Wait… I have to pay taxes on my Social Security?”

That reaction is common.

And understandable.

Most people spent decades paying into the system through payroll taxes. It feels intuitive that the benefit would come back tax-free.

Sometimes it does.

Often it doesn’t.

The difference comes down to a quiet little formula called provisional income.

And that’s where the surprise lives.

The Formula That Catches People Off Guard

Social Security taxation isn’t based solely on your benefit amount.

It’s based on this calculation:

Adjusted Gross Income (AGI)

- Tax-exempt interest

- 50% of your Social Security benefit

That total is your provisional income.

And it determines whether:

- 0% of your Social Security is taxable

- Up to 50% is taxable

- Up to 85% is taxable

Notice something subtle?

Even tax-exempt municipal bond interest counts in the formula.

That catches conservative retirees off guard.

The Thresholds (And Why More People Cross Them)

For married couples filing jointly:

- Over $32,000 → Up to 50% of benefits may be taxable

- Over $44,000 → Up to 85% may be taxable

For single filers:

- Over $25,000 → Up to 50%

- Over $34,000 → Up to 85%

Here’s the kicker:

These thresholds are not indexed for inflation.

They were set decades ago.

Which means every year, more retirees cross them.

Not because they’re wealthy.

Because inflation and RMDs push income upward.

“Up to 85% Taxable” Does Not Mean 85% Taxed

Important distinction.

If up to 85% of your benefit is taxable, that portion is included in your taxable income.

It does not mean you pay an 85% tax rate.

Example:

If you receive $40,000 in Social Security and 85% becomes taxable:

$34,000 is added to your taxable income.

It’s then taxed at your marginal rate.

Still meaningful.

But not catastrophic.

The Stacking Effect

Here’s where the real surprise happens.

Imagine this retirement income mix:

- $40,000 Social Security

- $40,000 IRA withdrawal

- $20,000 investment income

That IRA withdrawal doesn’t just add $40,000 of taxable income.

It can also cause more of your Social Security to become taxable.

So one dollar withdrawn may:

- Be taxable itself

- Trigger additional Social Security taxation

That creates an effective marginal rate that feels higher than your bracket suggests.

Retirees sometimes discover this after the fact — when the tax return arrives.

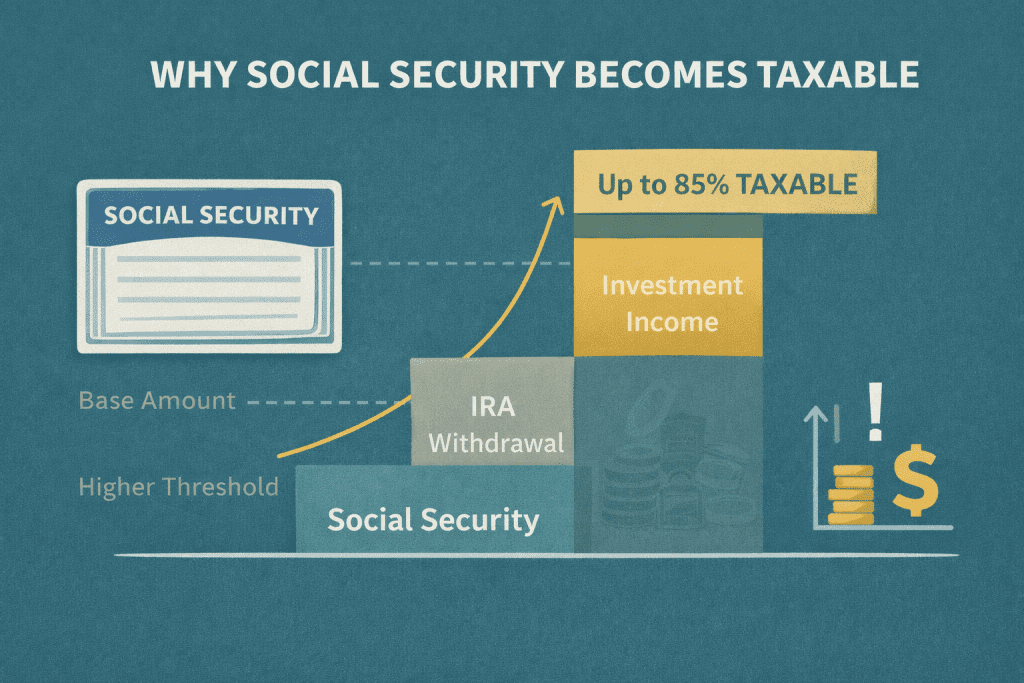

A Simple Example: How Social Security Becomes Taxable

Let’s walk through a realistic scenario.

Married Couple, Filing Jointly

- Social Security: $40,000

- IRA Withdrawal: $40,000

- Investment Income: $20,000

Step 1: Calculate Provisional Income

| Component | Amount Included in Formula |

|---|---|

| Adjusted Gross Income (IRA + Investments) | $60,000 |

| 50% of Social Security | $20,000 |

| Tax-Exempt Interest (if any) | $0 (assumed) |

| Provisional Income | $80,000 |

The key thresholds for married couples:

- Over $32,000 → up to 50% taxable

- Over $44,000 → up to 85% taxable

At $80,000 of provisional income, they’re well past the higher threshold.

Step 2: Determine Taxable Portion of Social Security

| Item | Amount |

|---|---|

| Total Social Security Benefit | $40,000 |

| Taxable Portion (up to 85%) | $34,000 |

| Non-Taxable Portion | $6,000 |

So instead of only taxing the IRA withdrawal and investment income, the tax return now reflects:

- $40,000 IRA withdrawal

- $20,000 investment income

- $34,000 taxable Social Security

Total Taxable Income from These Sources: $94,000

What Just Happened?

The $40,000 IRA withdrawal didn’t just add $40,000 of taxable income.

It caused:

- 85% of Social Security to become taxable

- An additional $34,000 added to taxable income

That’s the stacking effect.

This is why retirees sometimes feel like their “tax bracket” doesn’t tell the whole story.

The marginal impact of each withdrawal can be higher than expected because it triggers more Social Security taxation.

Why This Feels Surprising

Nothing dramatic happened.

No business sale.

No inheritance.

No lottery ticket.

Just normal retirement income sources interacting with a fixed formula.

And because the thresholds aren’t indexed for inflation, more retirees hit them every year.

The RMD Collision

For many retirees, the taxation shift happens when Required Minimum Distributions begin.

Early retirement might look tax-efficient:

- No RMDs yet

- Delayed Social Security

- Lower taxable income

Then:

- Social Security starts

- RMDs start

- Provisional income jumps

Suddenly, 85% of benefits are taxable.

Not because something went wrong.

Because income stacking accelerated.

The Widow(er) Shift

Here’s another quiet landmine.

When one spouse dies, the surviving spouse files single.

The income may not drop significantly.

But the thresholds do.

That can push more Social Security into taxable territory.

Combined with bracket compression, it’s a double impact.

This is one of the least discussed retirement tax transitions.

Where Planning Makes a Difference

You can’t always eliminate Social Security taxation.

But you can manage it.

Strategic levers include:

- Gradual Roth conversions before RMD age

- Coordinating Social Security start timing

- Managing IRA withdrawal sequencing

- Watching capital gain realization

The years between retirement and RMD age are often the most flexible.

Once RMDs begin, the train is harder to slow down.

The Real Surprise

The surprise isn’t that Social Security can be taxed.

The surprise is how easily ordinary retirement income triggers it.

You don’t need seven figures in taxable income.

You just need:

- IRA withdrawals

- Some investment income

- A few decades of inflation

That’s enough.

A Better Question

Instead of asking:

“Will my Social Security be taxed?”

Ask:

“How will my other income interact with my Social Security?”

That framing shifts the conversation from reaction to design.

Social Security taxation isn’t a flaw in the system.

It’s part of the architecture.

Understanding it early allows you to make decisions that feel intentional — instead of surprising.

And in retirement, fewer surprises are usually a good thing.