Quick Summary: If you retire before 65, Medicare isn’t there yet — and health insurance becomes one of your biggest planning variables. ACA premiums are based on income, not assets. Withdraw too much and subsidies shrink. Withdraw too little and you limit flexibility. The years between retirement and Medicare eligibility aren’t just a bridge — they’re a strategic window.

Retiring at 62 sounds great.

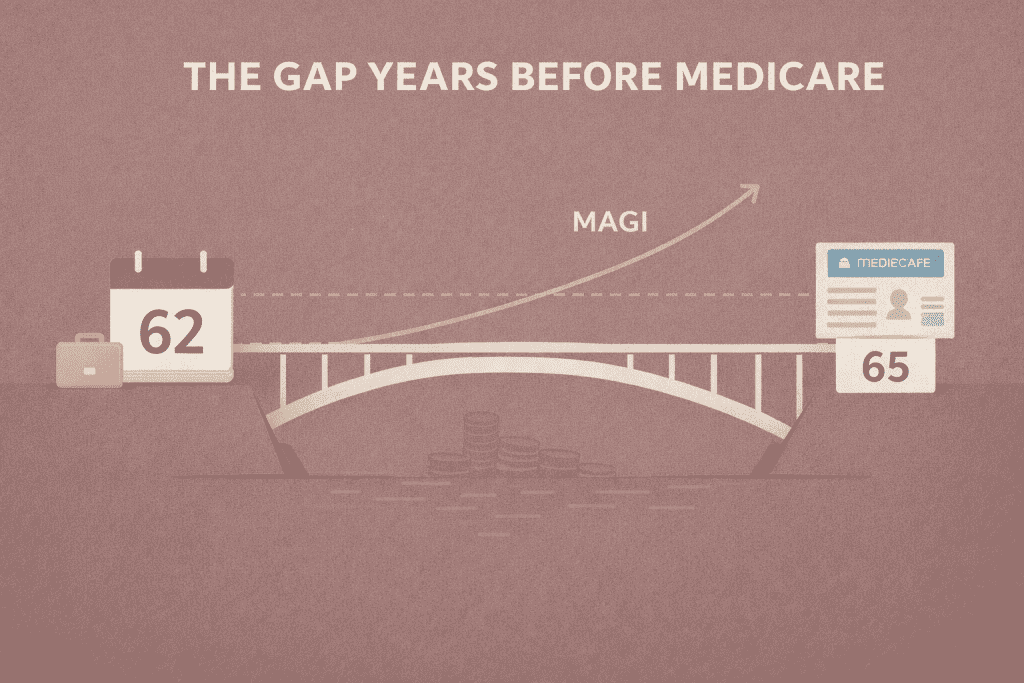

Until you remember Medicare doesn’t begin until 65.

That three-year gap — or five-year gap, or sometimes longer — is one of the most overlooked parts of retirement planning.

People obsess over:

- Social Security timing

- Roth conversions

- Withdrawal rates

But healthcare between retirement and Medicare?

That’s where real money can quietly leak.

The Myth: “I’ll Just Buy Insurance”

Yes, you can buy coverage.

But it’s not just about buying it.

It’s about how it’s priced.

If you retire before 65 and don’t have employer coverage, you’ll likely rely on the Affordable Care Act (ACA) marketplace.

And ACA premiums aren’t based on assets.

They’re based on Modified Adjusted Gross Income (MAGI).

You could have $2 million in investments.

If your income is low enough, you may qualify for premium subsidies.

You could also have a modest portfolio and lose subsidies because of one large withdrawal.

That’s the planning tension.

MAGI: The Number That Matters

For ACA purposes, MAGI generally includes:

- IRA withdrawals

- Capital gains

- Interest and dividends

- Roth conversions

- 1099 income

It does not include:

- Roth withdrawals

- Return of principal

- HSA reimbursements

Your healthcare cost during gap years is directly tied to how you manage that number.

The Subsidy Cliff (and Slope)

In recent years, the old “subsidy cliff” softened — but income still matters enormously.

As MAGI rises:

- Premium subsidies decrease

- Out-of-pocket exposure increases

- Total healthcare cost rises

This creates a strategic tradeoff.

Let’s say a couple retires at 62.

If they keep MAGI around a certain level, they may qualify for significant subsidies.

If they sell a large block of stock or convert too much to Roth in one year?

Subsidies can shrink fast.

The result:

Higher taxes.

Higher premiums.

Sometimes both.

The Roth Conversion Dilemma

Here’s where planning gets nuanced.

The early retirement years — before RMDs and before Social Security — are often prime Roth conversion years.

Lower income.

Lower brackets.

Flexibility.

But Roth conversions increase MAGI.

And higher MAGI can reduce ACA subsidies.

So now you’re balancing:

- Long-term tax optimization

vs. - Short-term healthcare subsidies

There isn’t a universal right answer.

There is sequencing.

Sometimes it makes sense to:

- Do moderate conversions

- Stay within subsidy sweet spots

- Spread conversions across multiple years

The gap years require coordination — not autopilot.

Capital Gains Can Sneak Up on You

Many retirees fund early retirement from taxable brokerage accounts.

Selling appreciated assets creates capital gains.

Capital gains increase MAGI.

Which can reduce subsidies.

That $80,000 withdrawal you thought was “mostly basis”?

It might still raise MAGI enough to change your premium bracket.

Healthcare planning during gap years isn’t just about spending.

It’s about how you source the spending.

HSAs: The Underused Tool

If you have a Health Savings Account from your working years, this is where it shines.

HSAs allow:

- Tax-free withdrawals for qualified medical expenses

- Reimbursement of prior medical expenses (if you kept records)

Using HSA funds during gap years can reduce the need for taxable withdrawals.

Which can help manage MAGI.

Which can help preserve subsidies.

That’s layered planning.

The Bridge Strategy

The gap years are temporary.

But mistakes during them can ripple forward.

Here’s what thoughtful planning often includes:

- Income Mapping

Project expected MAGI each year before Medicare. - Subsidy Modeling

Understand how income ranges affect premiums. - Conversion Sequencing

Spread Roth conversions strategically. - Asset Location Awareness

Decide which accounts to draw from first. - HSA Coordination

Use tax-free medical funds wisely.

These years are a bridge.

But they’re also an opportunity.

Once Medicare begins, subsidy strategy disappears.

That planning window closes.

A Simple Example

Couple retires at 62.

- Target spending: $90,000

- Investment portfolio: $1.5 million

If they structure income at $65,000 MAGI:

- They may qualify for meaningful subsidies.

If they structure income at $110,000 MAGI:

- Subsidies shrink significantly.

- Premiums rise.

Same spending.

Different sourcing.

Healthcare cost changes dramatically.

A Closer Look: How Income Changes Premiums

Let’s compare two scenarios for a retired couple, both age 62.

Target annual spending: $90,000

Portfolio: $1.5 million

Scenario A: Managed Income Strategy

| Category | Amount |

|---|---|

| MAGI | $65,000 |

| Estimated ACA Subsidy | Meaningful |

| Estimated Premium (after subsidy) | Lower |

| Roth Conversion Room | Limited but possible |

| Total Healthcare Cost | Moderated |

Scenario B: Uncoordinated Withdrawals

| Category | Amount |

|---|---|

| MAGI | $110,000 |

| Estimated ACA Subsidy | Significantly Reduced |

| Estimated Premium (after subsidy) | Much Higher |

| Roth Conversion Amount | Larger |

| Total Healthcare Cost | Substantially Higher |

When Scenario A Makes Sense (Preserve Subsidies)

Scenario A — managing MAGI carefully to preserve ACA subsidies — often makes sense when:

- Your traditional IRA balance is moderate, not massive

- Future RMDs aren’t projected to push you into much higher brackets

- You value lower healthcare premiums right now

- Cash flow certainty matters more than long-term tax smoothing

- You expect Social Security to cover a meaningful portion of future income

- You’re only 2–3 years from Medicare eligibility

In this case, the strategy is:

Keep income controlled.

Do smaller Roth conversions.

Preserve premium subsidies.

Revisit larger conversions after Medicare begins.

You’re prioritizing near-term efficiency and stability.

When Scenario B Makes Sense (Lean Into Conversions)

Scenario B — accepting higher MAGI and reduced subsidies in exchange for larger Roth conversions — may make sense when:

- Your traditional IRA balance is large and future RMDs look significant

- You’re projecting higher tax brackets later (especially after RMDs begin)

- You’re concerned about widow(er) bracket compression

- You want to reduce future IRMAA exposure

- You value long-term tax reduction over short-term premium savings

- You have several years before 65 to spread conversions out

In this case, the strategy is:

Accept higher healthcare costs now.

Convert more aggressively while you control timing.

Reduce future forced taxable income.

You’re prioritizing lifetime tax optimization.

The Balanced Middle Ground

Most retirees don’t live in pure Scenario A or pure Scenario B.

Often the smartest move is:

- Stay within a targeted MAGI “band”

- Do moderate Roth conversions

- Accept some subsidy reduction — but not total loss

- Adjust annually based on market returns and income needs

The key isn’t picking a side.

It’s understanding the tradeoff.

Because before 65, healthcare and tax planning aren’t separate decisions.

They’re connected.

And that connection is where good planning lives.

Same lifestyle.

Different sourcing.

Different healthcare costs.

The difference isn’t how much you spend.

It’s how that spending shows up as income.

That’s the gap-year planning tension.

The Emotional Side

Early retirement feels like freedom.

But healthcare uncertainty can create anxiety.

Understanding the system reduces that anxiety.

The goal isn’t gaming the system.

It’s understanding how income decisions affect premiums.

When you see the connection clearly, the planning becomes intentional — not reactive.

The Bigger Picture

Retiring before 65 isn’t just about having “enough.”

It’s about managing a moving target.

Healthcare in the gap years is:

- Income-sensitive

- Planning-sensitive

- Temporary — but expensive if ignored

Medicare will eventually simplify things.

Until then, income management and healthcare are linked.

Plan them together.

Because in retirement, the surprises you avoid are often more valuable than the returns you chase.

A Practical Note About Early Retirement Healthcare

ACA subsidy rules, income calculations, and premium structures can change over time. Individual income sources affect MAGI differently, and small changes in income can significantly impact healthcare costs. Before making major withdrawal or Roth conversion decisions during the years before Medicare eligibility, consider reviewing your plan with a qualified financial and/or tax professional who understands both retirement income strategy and ACA subsidy coordination.