A practical guide to filling the gaps in Original Medicare and tips on choosing a Medicare Supplement / Medigap Plan

Quick Summary

- Medicare Supplement plans (Medigap) help cover deductibles and coinsurance that Original Medicare leaves behind.

- Plans are standardized, meaning a Plan G from one company provides the same medical coverage as a Plan G from another.

- Most retirees choose Plan G or Plan N.

- The key decision is balancing monthly premium vs small out-of-pocket costs.

- Your Medigap Open Enrollment Period is the best time to enroll — insurers cannot deny coverage or charge more due to health conditions.

Why Many Retirees Buy a Medicare Supplement Plan

When people first enroll in Medicare, they quickly discover something important.

Medicare doesn’t cover everything.

Original Medicare (Parts A and B) leaves you responsible for deductibles, coinsurance, and other out-of-pocket costs. Original Medicare (Parts A and B) leaves you responsible for deductibles, coinsurance, and other out-of-pocket costs.

If you’re still getting oriented with Medicare itself, it’s worth first understanding how Medicare enrollment timing works.

That’s where Medicare Supplement insurance — usually called Medigap — comes in.

A Medigap plan helps pay those leftover costs.

The tricky part? The moment you start researching them, it can feel like you’ve wandered into a bait shop with 200 lures and no idea which one actually catches fish.

Different plan letters.

Dozens of insurance companies.

Premiums that vary widely.

The good news is that once you understand how Medigap actually works, the decision becomes much simpler.

What a Medicare Supplement Plan Actually Covers

A Medigap policy works alongside Original Medicare.

When you receive care:

- Medicare pays its share first

- Your Medigap plan covers some or all of the remaining costs

Depending on the plan you choose, this may include:

- Hospital coinsurance

- Medicare Part B coinsurance (typically 20%)

- Skilled nursing facility coinsurance

- Blood transfusions

- Foreign travel emergency coverage

- Some deductibles

The goal is simple:

more predictable healthcare costs in retirement.

Many retirees choose Medigap specifically because it reduces the chance of large or unexpected medical bills.

The Most Important Thing to Understand About Medigap

Here’s something many people don’t realize.

Medicare Supplement plans are standardized by the federal government.

That means:

A Plan G (or N, or any letter) from one insurance company provides the exact same medical coverage as a Plan G, N, etc from another company.

The coverage is identical.

The differences between insurers usually come down to:

- Premium price

- Customer service reputation

- Financial strength

- History of rate increases

Think of it like gasoline.

The fuel itself is the same — the price and the experience at the station may differ.

If you want to review the official details, Medicare provides a helpful overview in their Medicare’s official Medigap plan guide.

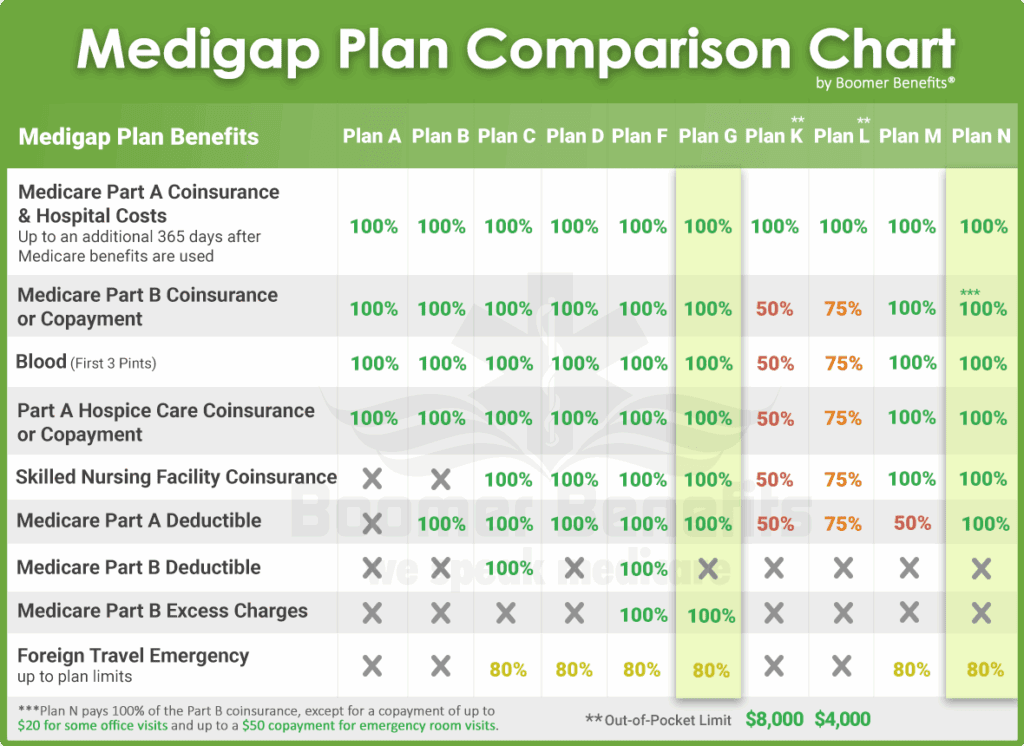

The Two Plans Most Retirees Choose

While there are several Medigap plan options, most retirees end up choosing one of two.

Plan G

Plan G is currently the most comprehensive option available to new Medicare enrollees.

It covers almost everything except the Medicare Part B deductible, which is $283 for 2026 (and subject to annual increases; it was $257 in 2025).

Once that deductible is paid, Plan G typically covers nearly all remaining Medicare-approved expenses.

Why many retirees choose it:

- Very predictable healthcare costs

- Minimal out-of-pocket exposure

- Accepted nationwide by any provider who accepts Medicare

For people who want simplicity and peace of mind, Plan G is often the default choice.

Plan N

Plan N offers lower premiums in exchange for a small amount of cost sharing. Depending on your location, the premium difference can be significant.

With Plan N, you may pay copays of:

- Up to $20 for certain doctor visits

- Up to $50 for emergency room visits (if not admitted)

Importantly, the key words here are, you MAY pay, and UP TO copay limits. $0.00 is also a copay up to $20. In my personal experience (my wife and I both have Supplement Plan N), we rarely get charged a copay. This can vary by your location and provider. The highest copay we’ve ever had is $14.

Plan N also does not cover Part B excess charges, although these are very is capped at 15% of Medicare-approved charges, which can be significantly lower than what a provider charges someone without insurance. Again, my wife and I have never been charged an excess charge. It’s also important to understand that the excess charge amount is limited to 15% of Medicare-approved charges, which can be significantly lower than what a provider charges someone with no insurance.

Why some retirees prefer it:

- Lower monthly premium

- Protection from major medical expenses

In simple terms:

Plan G trades higher premiums for fewer medical bills.

Plan N trades lower premiums for occasional small copays.

Interested in getting new articles in your email?

Why Plan F Is No Longer Available to Most New Enrollees

You may still hear people talk about Medicare Supplement Plan F, which historically covered every Medicare cost.

However, Plan F is no longer available to people newly eligible for Medicare after 2020.

Some retirees who enrolled earlier still have it, but most new beneficiaries choose Plan G instead, which provides nearly identical coverage.

How to Choose a Medicare Supplement Plan

Once you’ve selected the plan letter that fits your needs, the next step is choosing the insurance company offering it.

Since the coverage itself is standardized, the decision typically comes down to a few practical factors.

Compare premiums

Prices can vary widely between insurers — even for the exact same plan.

However, the lowest price today isn’t always the best long-term choice.

Some companies start with low premiums but raise them aggressively over time.

Look at rate increase history

Medigap premiums usually increase as you age.

Companies with a history of moderate, predictable increases may be a better long-term fit than those known for sharp jumps.

Your Medicare broker should be able to provide you with the premium-increase history for any provider they carry. If not, consider finding a new broker.

Consider company reputation

It’s worth choosing insurers with:

- Strong financial ratings

- A long history offering Medigap plans

- Reliable customer service

A licensed Medicare broker can often help compare these factors across companies.

PERSONAL NOTE: There are thousands of Medicare brokers out there. Some are terrific, some are not-so-swift, and some only want to sell you whatever pays them the most commissions. My wife and I both used Boomer Benefits as our Medicare Broker. Their agents are paid a salary, so they have no commission income to influence what they recommend. They also provide amazing support both before and after the sale, which few brokers do. As with many Medicare brokers, their services cost you nothing. This isn’t a recommendation; you should choose. a broker you are comfortable with.

Don’t Miss Your Medigap Open Enrollment Window

Timing matters.

Your Medigap Open Enrollment Period begins when you:

- Are 65 or older, and

- Enroll in Medicare Part B

This six-month window is important because:

- You cannot be denied coverage

- You cannot be charged more due to health conditions

Outside this window, insurers in most states can require medical underwriting.

In other words, waiting too long may make it harder to change or obtain coverage later.

Practical Note

Medicare decisions are personal and can have long-term financial implications. Plan availability, pricing, and underwriting rules can vary by state and insurer.

Before enrolling, it can be helpful to review your options with a licensed Medicare advisor or through the State Health Insurance Assistance Program (SHIP), which provides free, unbiased guidance.

You can find your local SHIP program here.

Bottom Line

Medicare Supplement plans exist for one main reason:

to make healthcare costs in retirement more predictable.

Once you understand that Medigap plans are standardized, the decision becomes far less complicated.

Choose the plan letter that fits your comfort level.

Then choose a reputable insurer with competitive pricing.

And you can spend less time worrying about healthcare bills — and more time enjoying retirement.

Medicare Supplement FAQs

What is the best Medicare Supplement plan?

The most common Medicare Supplement plans for new enrollees are Plan G and Plan N. Plan G offers the most comprehensive coverage after the Medicare Part B deductible, while Plan N typically has lower monthly premiums but includes small copays for certain doctor and emergency room visits.

For many retirees, the choice comes down to whether they prefer slightly higher premiums with minimal out-of-pocket costs (Plan G) or lower premiums with occasional copays (Plan N).

Can you see any doctor with a Medicare Supplement plan?

Yes. Medicare Supplement plans work with Original Medicare, which means you can see any doctor or hospital in the United States that accepts Medicare.

Unlike many Medicare Advantage plans, Medigap policies do not use provider networks, giving retirees much greater flexibility when choosing doctors and specialists.

Are Medicare Supplement plans the same with every insurance company?

Yes. Medicare Supplement plans are standardized, meaning a Plan G from one insurance company provides the same medical coverage as a Plan G from another.

The main differences between insurers are typically:

- Monthly premium

- Customer service

- Financial strength

- Rate increase history

Because of this standardization, comparing companies is largely about price and reputation, not coverage differences.

When should you enroll in a Medicare Supplement plan?

The best time to enroll is during your Medigap Open Enrollment Period, which begins when you are age 65 or older and enrolled in Medicare Part B.

During this six-month window, insurance companies cannot deny coverage or charge higher premiums because of health conditions, making it the easiest time to choose a plan.

Can you switch Medicare Supplement plans later?

In many states, switching Medicare Supplement plans later may require medical underwriting, meaning insurers can review your health history before approving coverage.

Because of this, many retirees choose their Medigap plan carefully when they first enroll in Medicare.

Some states provide additional consumer protections that make switching plans easier.

2 comments

I turn 65 in May of this year, so I knew I had to get started. I consider myself a DIYer, so I began doing my own research. I’m a smart guy, but the more research I did, they more confused and stupid I felt. The best thing I ever did was connect with a reputable insurance agent (ABT Insurance, in my case), and threw away every piece of mail I received soliciting medicare insurance. After a few phone calls with the agent, and my rapid fire questions, I was finally feeling I could make an informed decision. I first discovered that by living in California, there is a unique feature known as the ‘birthday rule’, which is essentially a true open enrollment period established around your birthday that will allow you to switch to equal or lesser plans without underwriting — not sure I would have ever discovered that on my own! I whittled my choices down to Kaiser Permanente’s Advantage plan (they are my current insurer) which had a low maxium out of pocket less than $3K, and a high deductible plan G with a similar MOOP. I already had the ‘evidence of coverage’ from Kaiser, and I asked my insurance broker to send me the same for my top three Plan G-HD providers, and I read them. I went with the Plan G-HD. Similar to your “buying gasoline” comment (I actually used that same example when I was talking to my broker…great minds), I based my choice of insurers based upon premium price, premium increase history, and preauthorization trends. Nothing else mattered. Side note, I actually found the Medicare website to be very helpful in selecting my Plan D including entering in my current perscription drugs. I also found the website accurately displayed the premuims of the varioius medigap policies. So much so, I was able to have those in fornt of me when speaking with my agent. Now, onward to selecting all new medical practioners and getting new perscriptions written for my current medications. Hmm, maybe Kaiser will transfer those. I guess I should find out. Wish me luck! And oh yeah, MOOP is an acronym for Maxium Out Of Pocket…one of many new terms I have learned in the proccess and can’t wait to forget.

Abt Insurance: https://abtinsuranceagency.com/

Thanks for the great comment, Tim!

I bet tossing all that solicitation mail was exhausting… It’s crazy how many emails, texts, phone calls, and mail happen during this time.

Sounds like you’re on a great path! Best of luck to you!